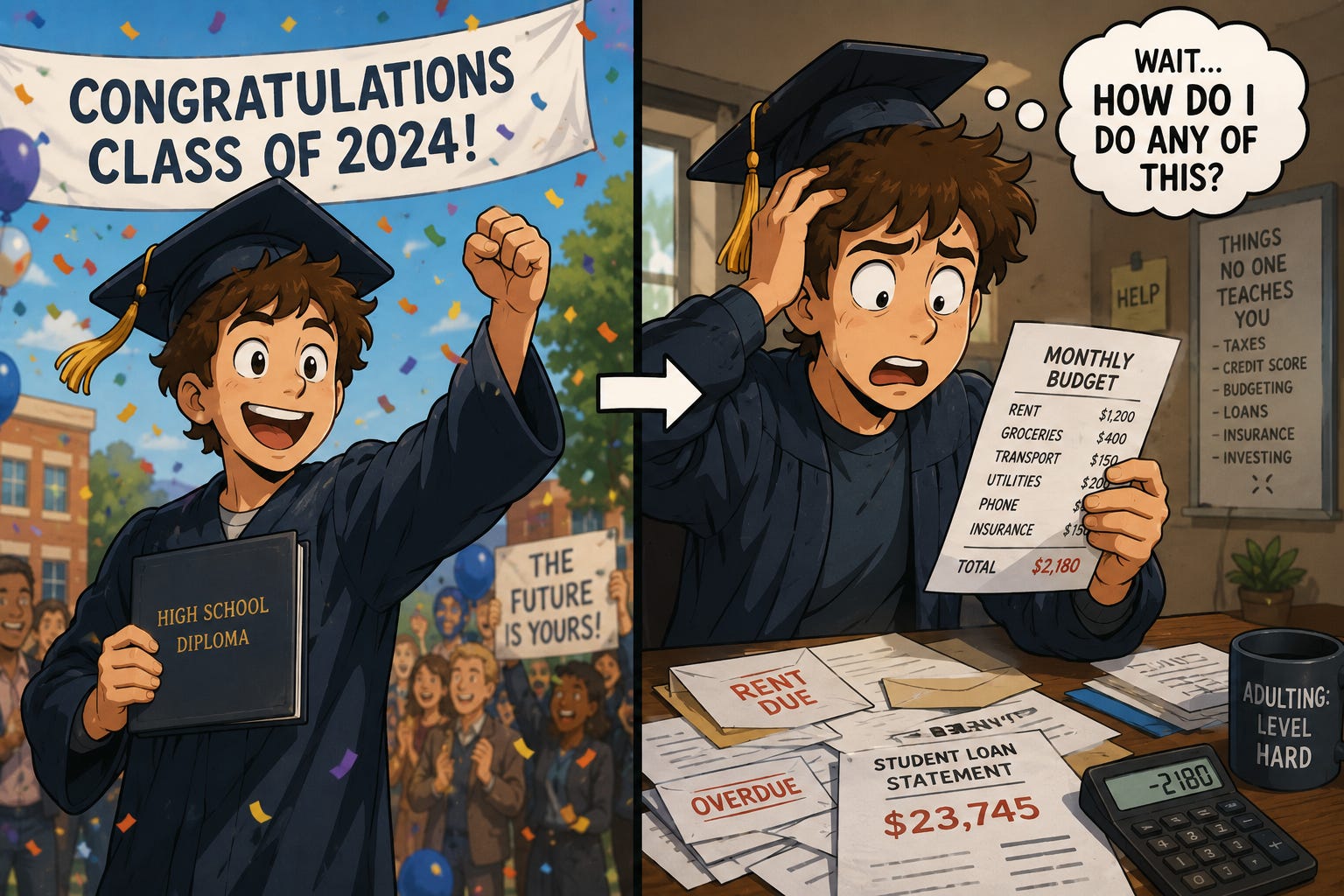

Financially Illiterate

Knowledge, much like interest, compounds.

Trisha Jha recently wrote an excellent article about the push to explicitly include financial literacy in F-2 Mathematics to improve levels of financial literacy in Australia. Which explored in depth the idea that in Australia many individuals manage to go through schooling without ever gaining basic education about financial concepts such as Inflation, Interest Rates and Taxation.

I am first and foremost a teacher of Humanities and my areas of specialisation are in Economics and Business. More and more each year I am finding that my students do not have a basic understanding of almost any economic concepts by the time they get to my classroom. This is challenging on a number of levels. Firstly, it feels like a failure of the school system to prepare these students for the outside world. Economics is a subject in Victoria which only approximately 3,000 students undertake each year which is a miniscule fraction of the overall student body and therefore the majority are not going to gain the financial literacy the subject provides. Secondly, it means that the depths of understanding which can be created and developed throughout the two year course are limited as we are starting from a near zero baseline and building from there.

It would be similar to having two people wanting to run a sub 20 minute 5km time trial. One runner has been playing competitive sports their whole life and the other has never ran a day in their life. The goal is definitely achievable for both parties but it is going to take one of them a whole lot longer.

Curiously, in our Victorian Curriculum 2.0 (the context in which I teach1) the following is stated in the guidance around financial literacy and where it appears in the curriculum:

the Economics and business learning area, students progressively build financial literacy skills from Levels 5 to 10. At Levels 5–6, they learn about everyday financial decision-making, opportunity cost, and factors influencing consumer choices. In Levels 7–8, students explore consumer rights and responsibilities and develop budgeting and goal-setting skills. By Levels 9–10, they engage with financial planning and investment strategies to prepare for adult financial responsibilities

the Mathematics learning area, financial literacy is represented by students’ ability to apply numerical skills to real-world financial contexts.

Let’s tackle Maths first.

'Is represented by the students ability to apply numerical skills to real-world financial contexts' is an incredibly vague statement to make when it comes to building clear financial literacy. Are we expecting students to develop the knowledge of financial literacy elsewhere and then bring it to math? Because that alone is fraught with our next set of issues.

The way in which financial literacy is suggested to be embedded within the Humanities is particularly tricky. Humanities from grades 5 to 10 tend to be a conglomeration of Geography, Economics, History, Civics and Social Studies in Australia. Further to that, for the most part teachers plan and implement their interpretation of the curriculum in schools either individually or in teams. These teachers themselves are individuals who have gone through the education system without ever gaining the financial literacy that they themselves require in adult life and yet they are the ones being tasked with building the knowledge of the future generation.

The problem is, generalist teachers tend to favour the content which they have a specialty in as they are comfortable in their ability to teach it well. Therefore geography and history tend to take centre stage in these humanities units as teachers feel most competent in bringing these to life in their classroom. Meanwhile, economics gets pushed further and further down the line. Concepts may be briefly touched on, but rarely in a meaningful way or retrieved at intervals required to build in depth long term memory.

Despite being a specialist economics teacher now, I remember hating studying economics in high school because I didn’t have the background knowledge to actually understand the content. There was no schema to attach concepts such as inflation to because I had never had the opportunity to build this understanding.

Much in the same way we expect students at some point to learn about Parliament, how laws are made and the democratic process to become informed voters of the future, the same should be true of the economy and therefore financial literacy.

How are we supposed to know who to elect when the May budget is just a series of statements made by a man in a suit most of which only indirectly impact you and barely in a way you’d notice without paying particular attention?

In Natalie Wexler’s 'The Knowledge Gap' this phenomenon was explored in noticing that when the school day is stuffed to the brim with more and more things which need to be met. That often it is the humanities education that is then glossed over in favour of literacy and numeracy programs. The irony here being that without the contextual understanding that the humanities brings, students may struggle to understand the content they’re now literate enough to read.

Additionally, much of the Economics and Business knowledge within the strands aligns with Year 9 and Year 10 where many schools have these subjects operate as optional electives for students which means that if they do not opt-in to learn about inflation and taxes2 . Further to that, many schools then end up going a little bit rogue and structuring these subjects as ‘mini VCE’ units despite that never being the intention. This again means that some of the core base information important for general financial literacy may never be learned by the students.

In the recent How Learning Happens session I attended by Dr Carl Hendrick he demonstrated this emphatically through showing the attendees the first passage of Dr Jeckyll and Mr Hyde. Inclusive of statements such as “to mortify a taste for vintages” which independently is a series of words which may would know the definition of individually, however together in context takes on a whole other meaning which is reliant on a deeper background knowledge of history and the writing of the time.

Despite this example definitely not being relevant to financial literacy (although to be fair I have not read further into the story to find out) the way in which background knowledge is cumulative and benefits learners as they progress through their years of education persists.

Let’s get back to the guidance from the Department of Education… how should we teach financial literacy?

Research suggests that scenario-based, applied learning and ‘real world’ problem solving foci in student learning experiences are most likely to support learning progress (Amagir et al. 2017).3

AAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAHHHHHHHHHHHHH.

Departmental Red Flags ahoy!

This is your bi-monthly4 reminder that not all research is equal and that none of the above can occur without a rich knowledge of financial literacy being created first.

The above is a snippet of the VCE Foundation Maths Unit 3 curriculum which pretty explicitly builds student capacities when it comes to financial literacy.

The problem?

Not all schools either offer Foundation Maths and may only offer General Maths, Methods and Specialist instead where $ symbols are replaced with all of the letters of the alphabet.

Then if we start exploring further back into the F-10 Maths curriculum we can only really find the financial literacy if we explore the elaborations such as the following:

use mathematical modelling to solve practical problems involving additive situations, including simple money transactions; represent the situations with diagrams, physical and virtual materials; use calculation strategies to solve the problem(VC2M1N05)

ELABORATION:

modelling simple money problems involving addition and subtraction using whole dollar amounts; for example, setting up a shop and role-playing practical problems of buying and selling goods, using addition and subtraction with play money and prices in whole dollar amounts; or solving the problem ‘I had $14 and was given $15 for my birthday’ using addition to answer the problem

This is from the level 1 curriculum and seems to be the first explicit reference to financial knowledge in the Victorian Curriculum. Here it is essentially addition and subtraction with simulated money problems. Which to be fair, is very much age appropriate and in line with their development of mathematical understanding as well as the context in which they’d be interacting with the economy. For a 6 year old in Grade 1 you could definitely argue that their main need for financial literacy is “I have 5 dollars and frozen yogurt at the canteen is 3 dollars”.

Next we skip ahead to the level 8 curriculum:

solve problems involving the use of percentages, including percentage increases and decreases and percentage error, with and without digital tools

VC2M8N05

ELABORATIONS

This may involve students:

using percentages to solve problems, including those involving mark-ups, discounts and Goods and Services Tax (GST)

The word ‘may’ is doing some heavy lifting for financial literacy there. It easily may not involve that. It may involve it in a single worded problem, or many over time. It is inviting a level of variance which could greatly impact the future of students and their financial stability. Not only this, the inclusion of financial literacy at all at the year 10 level requires either the teachers resources to have explored this elaboration or for the teacher to have done it themself.

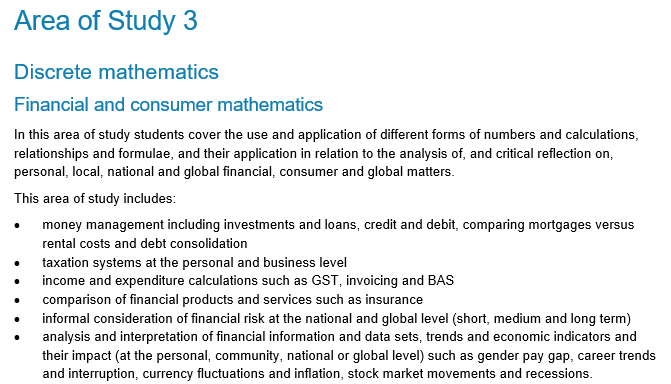

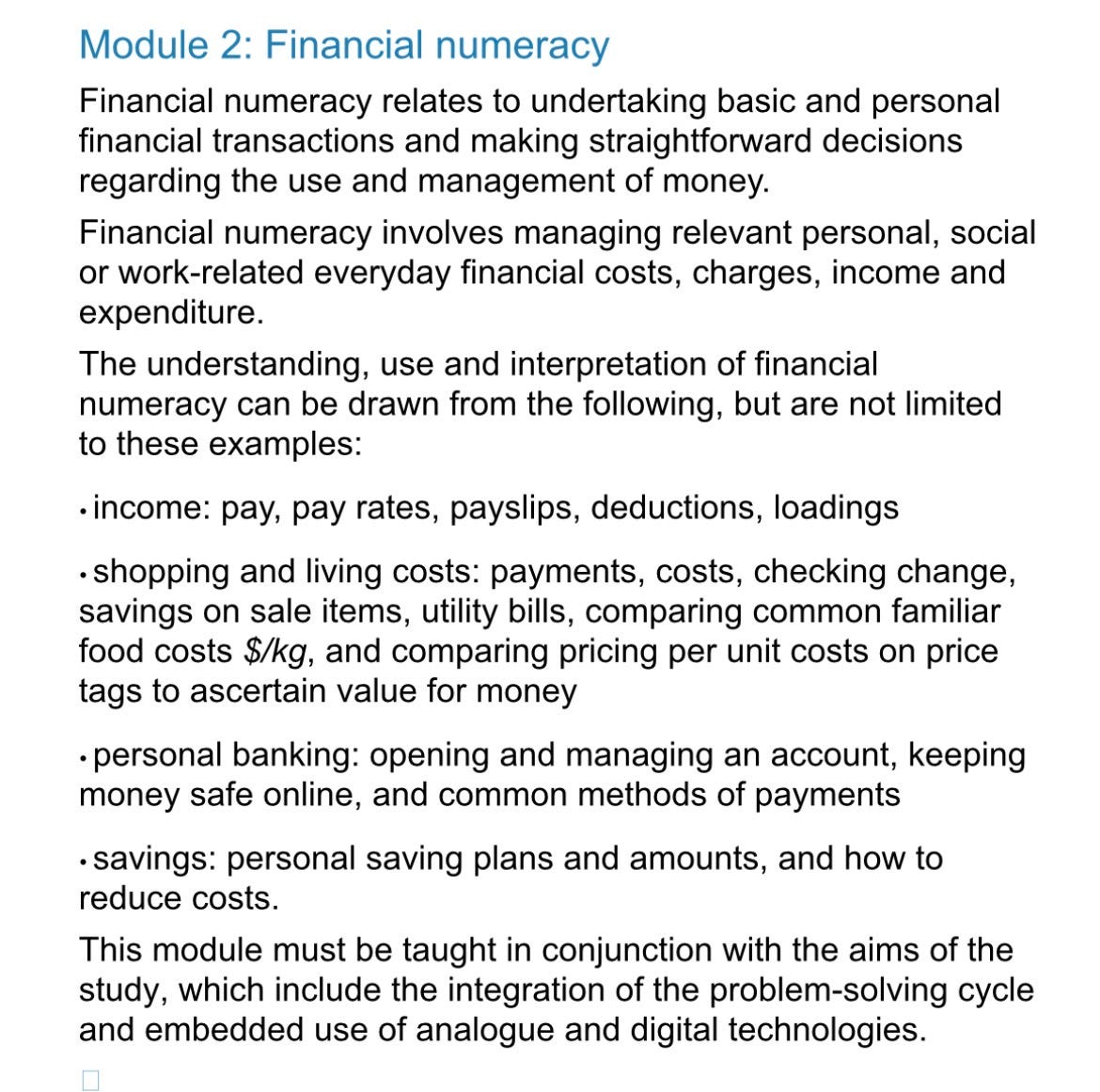

In my deep dive into financial literacy curriculum in schools I next decided to look at our two other potential pathways for students at a senior level. The two applied learning strands of the VPC and VCE-Vocational Major certificates.

The VPC Unit 3 numeracy seems to outline an incredibly practical set of knowledge and skills which would benefit any young adult and it seems a little bit counterintuitive that the larger majority of students would miss out on this as only a very small percentage of schools offer the VPC at all.

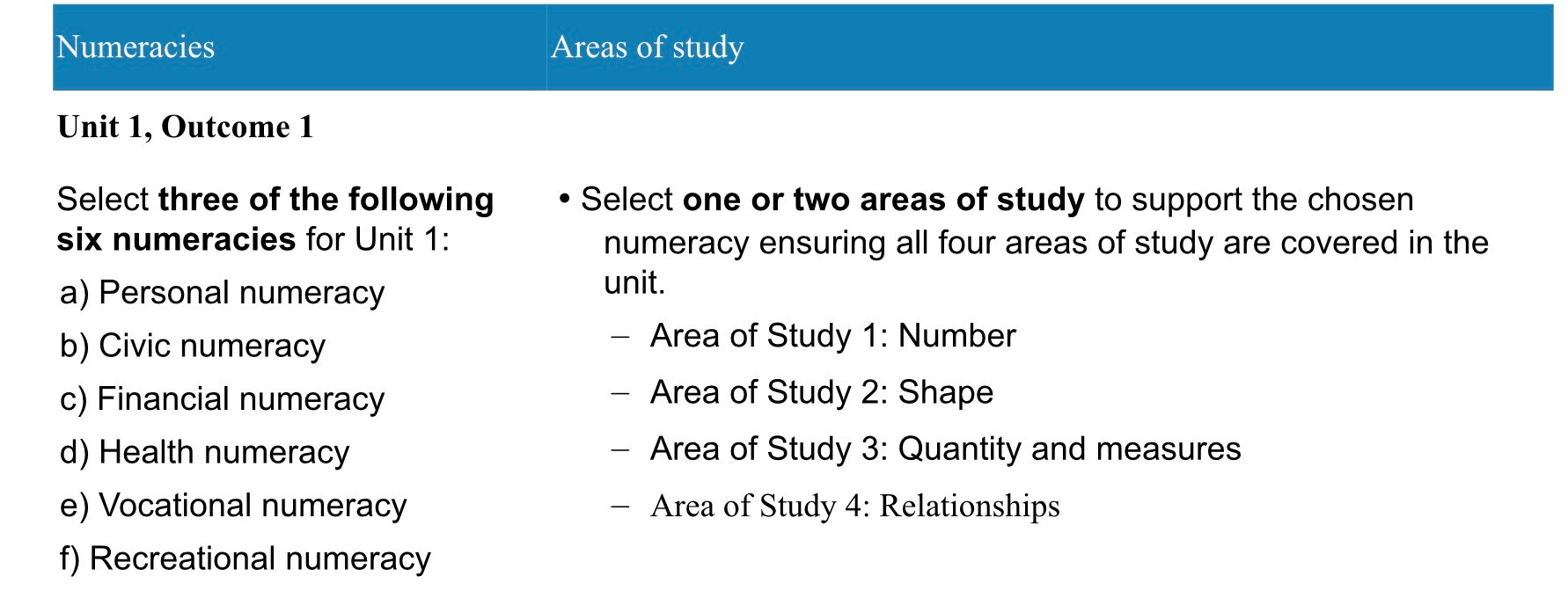

The VCE-VM on the other hand offers up some bonkers curriculum design where it is set up as a choose-your-own-adventure of numeracy. Technically in this design you could lead financial literacy via the shapes area of study. This just seems like a recipe for incredibly high variance in the quality of financial literacy instruction delivered in schools offering the course based almost solely on teacher quality, teacher judgment or the bought curriculum materials they are accessing.

Does adding compulsory ‘financial literacy’ content at a F-2 level in addition to what already exists solve these problems?

Well that really depends.

Some degree of understanding of money when learning about maths operations is great. E.g. If Tommy works for 4 hours shifts and earns $20 per hour how many shifts would Tommy need to work to purchase a $400 bike?

This would have legitimate positive impact on the students understanding of finances and budgeting. However, the way in which financial literacy is sequenced throughout the curriculum would need to be very carefully considered.

Knowledge around taxes become incredibly relevant to students around 14 and 15 years of age and therefore it makes a lot of sense to be embedded in the curriculum around this age. Furthermore, the knowledge around credit, interest rates, inflation all have a substantial impact on students once leaving school and turning 18 years of ages and therefore some mandatory inclusion in years 11 and 12 would greatly benefit students in their adult years.

All I know is that despite these concepts clearly being embedded in the curriculum at different levels, financial literacy somehow seems to evade the average student across their educational journey. This is an issue not only for the future financial stability and decision making of those students as they enter adulthood but also a failing of the checks and balances auditing our guaranteed and viable curriculum and how it is applied in schools.

I don’t think that sprinkling more financial literacy into the F-2 curriculum is going to fix what appears to be more of a systems issue.

None of this is to say that financial literacy isn’t occurring at all within schools. I am more attempting to highlight the ‘one-off’ or tokenistic nature of its inclusion. A history unit may involve a passing reference to hyperinflation in Germany, with no in depth exploration of what that means. Further to that, we forget 60% of what we’ve learned within 9 hours. I would hazard a guess that after that hyperinflation mention is unlikely to be retrieved and rehearsed with meaningful detail.

Financial literacy needs to be in the curriculum, but it needs to be mandatory, sequential and retrieved at meaningful intervals at a time when it is developmentally appropriate.

Teaching a 6 year old about inflation should really be limited to balloons.

The only credit I need my daughter to know about in grade 1 is the sleep debt she owes to us.

All of this financial literacy curriculum really boils down to a quote from Caiti Wade I find myself using in its infinite usefulness in many contexts.

If it feels optional, it is optional. - Caiti Wade

Although as we venture into the classic Melbourne winter the allure of teaching up north grows stronger.

Who could imagine a student not picking this subject over something like outdoor ed or drama?

Amagir A, Groot W, Maassen van den Brink H and Wilschut A (2017) ‘A review of financial-literacy education programs for children and adolescents‘, Citizenship, Social and Economics Education, 16(1):56–80.

Here’s hoping that your bi-monthly is twice a month and not every two months.

As you know Shaun, I will argue for all of this, just as I believe Civics and Citizenship is tragically underrated in the implementation. Sadly we have too many voices competing with us at this moment in time. What sane person says that financial literacy isn’t important? Recently I have written a Year 8 unit for consumer rights and protections. These rights are fundamental to get the most out of those spent dollars that are hard earned. Yet I couldn’t help thinking that if we teach this unit well, make connections with real world examples, stimulate problem solving thinking, etc that’s great for our students. Yet I know that our area is not deemed important by many, in preference of History and Geography. We need a much more balanced Humanities curriculum with genuine accountability. NSW do it through the school certificate (which is far from perfect). It is at least an attempt to hold schools at little accountable for History and Geography and integrated Civics and Citizenship. If it was more balanced across the nation, including Economics and Business, as four equal strands, then I believe we’d deliver better real world student outcomes. Given that we need the Commonwealth to drive this, to actually get the states to work together, I think I’ll be disappointed for sometime yet. Don’t give up though. Maybe our passion might help one day.

After I hit publish on Tuesday's post one of the thoughts I had was that I was trying to teach Year 10 students about hyperinflation in Weimar Germany without many of them necessarily understanding what 'inflation' is. Cue mumbling about the money supply and too much chasing too few goods while they stared at me blankly.